Every corporate milestone has its inflection point. For Indian HR and payroll teams, that point is happening right now.

As we cross into the mid-2026 filing window, enterprises find themselves operating in a unique dual-reality. On one hand, payroll desks must close out the historical Financial Year (FY 2025–26) using the familiar legacy compliance formats. On the other hand, every single payroll run executed since April 1, 2026, is governed by a completely rewritten architecture: Tax Year 2026–27, driven by the Income Tax Act, 2025.

For leadership, managing this transition isn’t just about changing system labels; it is about re-engineering how data flows from your internal ERPs to the government portals. Here is your executive blueprint to auditing, transitioning, and executing compliance without operational friction.

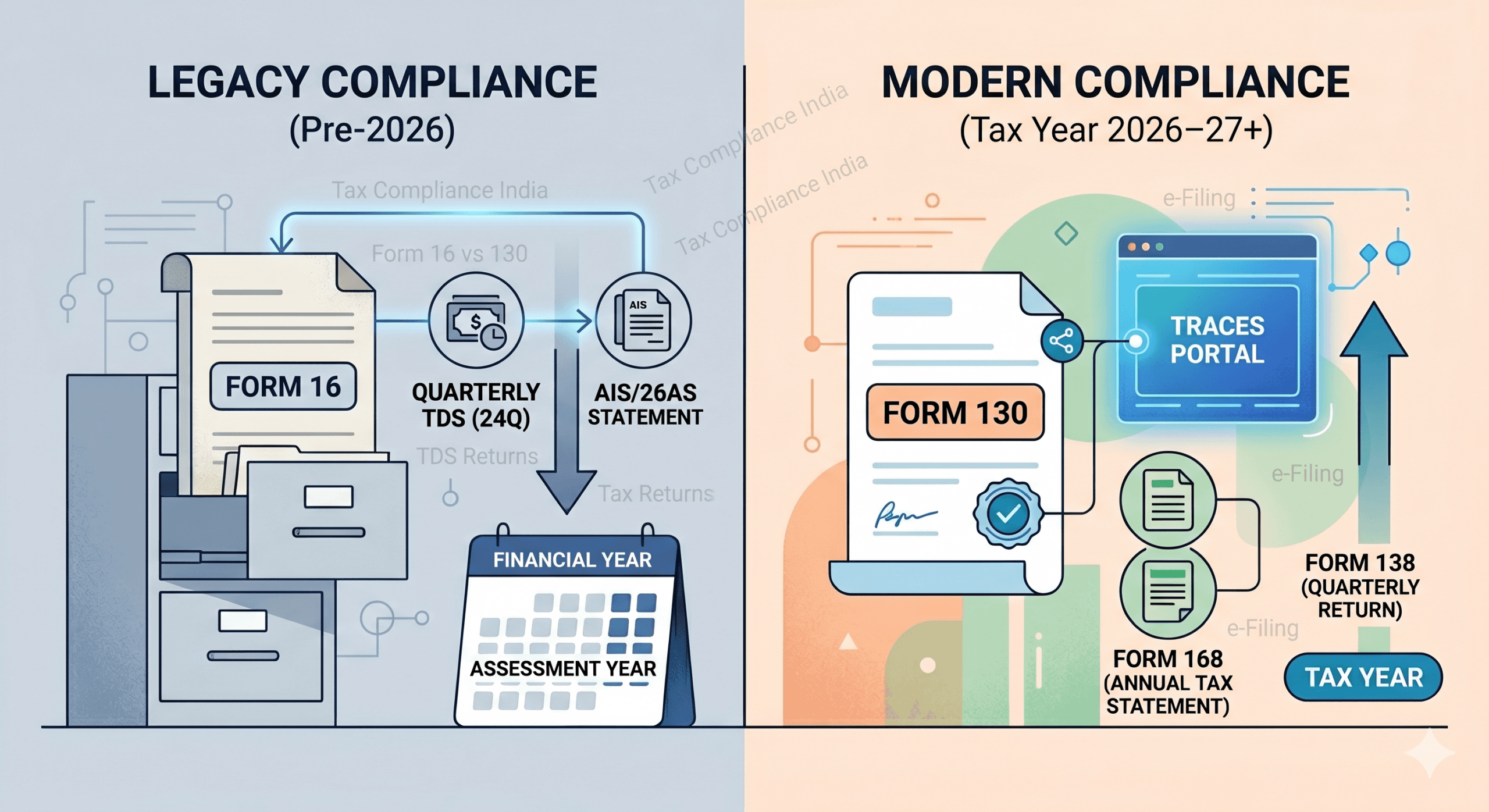

1. Managing the Dual-System Overlap (Mid-2026)

The biggest immediate operational risk is process confusion. Because the transition occurs mid-year, your payroll team is effectively running two distinct regulatory regimes simultaneously.

To ensure absolute clarity and prevent filing data corruption, your execution desk must maintain a strict firewall between historical filings and active operational cycles:

- The Historical Track (FY 2025–26): For the filing window closing mid-2026, your team will continue to issue the legacy Form 16 and file Form 24Q. This covers the previous financial cycle.

- The Active Track (Tax Year 2026–27): For all salary distributed, bonuses paid, and tax withheld from April 1, 2026, onward, the legacy system is officially retired. The mandatory compliance outputs are now Form 138 (Quarterly Return) and Form 130 (Annual Certificate).

Leadership Action Item: Ensure your internal accounting and HRIS platforms do not accidentally overwrite legacy data schemas when upgrading your software to support the new Tax Year 2026–27 configurations.

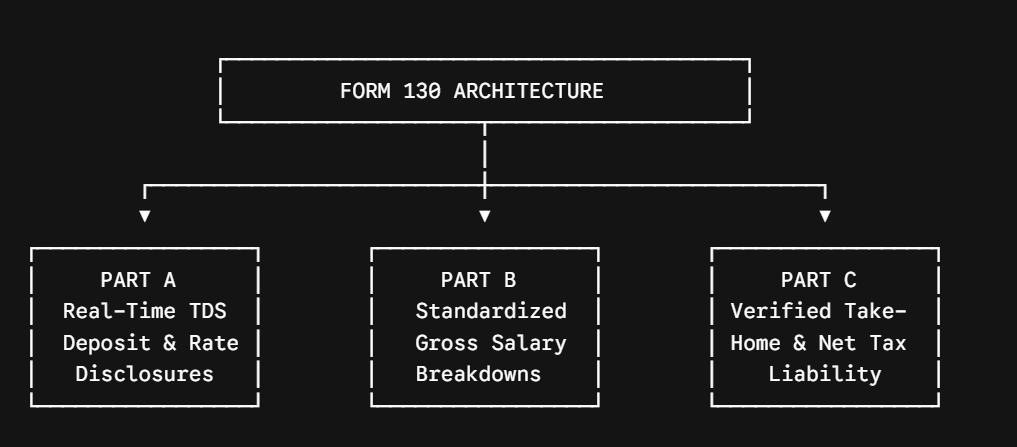

2. Deconstructing the Form 130 Three-Part Architecture

The shift from Form 16 to Form 130 is structurally profound. The old Form 16 separated portal-derived tax deposits (Part A) from your internal company calculations (Part B), which often led to mismatched data and manual reconciliation nightmares.

Form 130 solves this by introducing a fully unified, system-verified Three-Part Architecture generated directly via the TRACES portal:

📋 Part A: Real-Time Verification & Rate Disclosures

Part A pulls directly from central government deposits. Crucially, it now mandates the disclosure of the exact tax deduction rate percentage. If a high-earning employee’s special allowance or performance bonus was accidentally calculated at an incorrect slab rate by your internal system, the discrepancy will be immediately visible on the face of the form.

📋 Part B: Standardized Salary & Exemption Mapping

Part B provides a granular breakdown of gross salary, perquisites, and profits in lieu of salary. Under the Income Tax Rules, 2026, these fields are rigidly mapped to the streamlined codes of the new Act. Manual workarounds or custom line items that your payroll software used to generate are no longer permitted.

📋 Part C: The Reconciliation Anchor

Part C is the final ledger. It maps total tax due against total tax deposited, establishing the definitive net tax liability or refund status. Because Parts A and B are tightly bound to the digital ecosystem, Part C acts as an auto-reconciled stamp, effectively eliminating the year-end “mismatch panic” that traditionally flooded HR desks with employee inquiries.

3. Tech Stack Audit: Is Your Vendor Truly Ready?

Many legacy Enterprise Resource Planning (ERP) tools and local payroll vendors claim they are “updated” when they have simply updated text headers. A true structural update requires deeper programmatic integration.

CHROs should immediately issue a Compliance Readiness Questionnaire to their payroll technology partners, demanding verification on three non-negotiable capabilities:

1. Section 392 API Mapping

Does the payroll software route current monthly withholding logic through Section 392 of the Income Tax Act, 2025 (which supersedes the legacy Section 192)? If the software is still referencing old section codes, your quarterly filings will fail validation.

2. Form 138 Seamless Export

Can the system seamlessly export text and data schemas configured exactly for Form 138 (the new quarterly salary TDS return)? Any structural errors here will stall your submissions, creating a domino effect that blocks the eventual generation of employee certificates.

3. Real-Time TRACES Integration

How does the software interface with TRACES? Look for automated validation loops that flags rate mismatches before the quarterly submission is locked in, saving your team hours of corrective filing later.

Turn Regulatory Transition Into an Enterprise Advantage

Structural regulatory shifts of this scale naturally introduce friction, but they also present an incredible opportunity to modernize your corporate administration.

By upgrading your technology stacks, aligning your finance and HR operational desks, and proactively educating your workforce on what to expect when they view their new Form 168 (Annual Tax Statement), you protect your enterprise from compliance lockouts and administrative gridlock.

Navigating this new era of Indian corporate compliance requires precision. Ensure your leadership team is equipped with the right tools, verified software updates, and clear execution strategies to stay ahead of the curve in Tax Year 2026–27.