Every year like clockwork, corporate HR and payroll departments execute a familiar script. Come May and June, teams sit down to compile salary details, reconcile quarterly returns, and issue Form 16 certificates to their workforce. It has been a standard operational routine across corporate India for generations.

But that routine has just been rewritten.

With the wholesale implementation of the Income Tax Act, 2025 and the Income Tax Rules, 2026 taking effect for Tax Year 2026–27, India’s direct tax architecture is undergoing its most radical transformation since 1961. The old numbering frameworks have been systematically phased out to make way for a streamlined, data-driven system.

At the very front of this regulatory shift is the retirement of Form 16 and the introduction of its direct successor: Form 130.

For Chief Human Resources Officers (CHROs), payroll directors, and enterprise founders, this is not a cosmetic label change. It represents a fundamental structural modification in how payroll compliance is structured, validated, and communicated to your workforce.

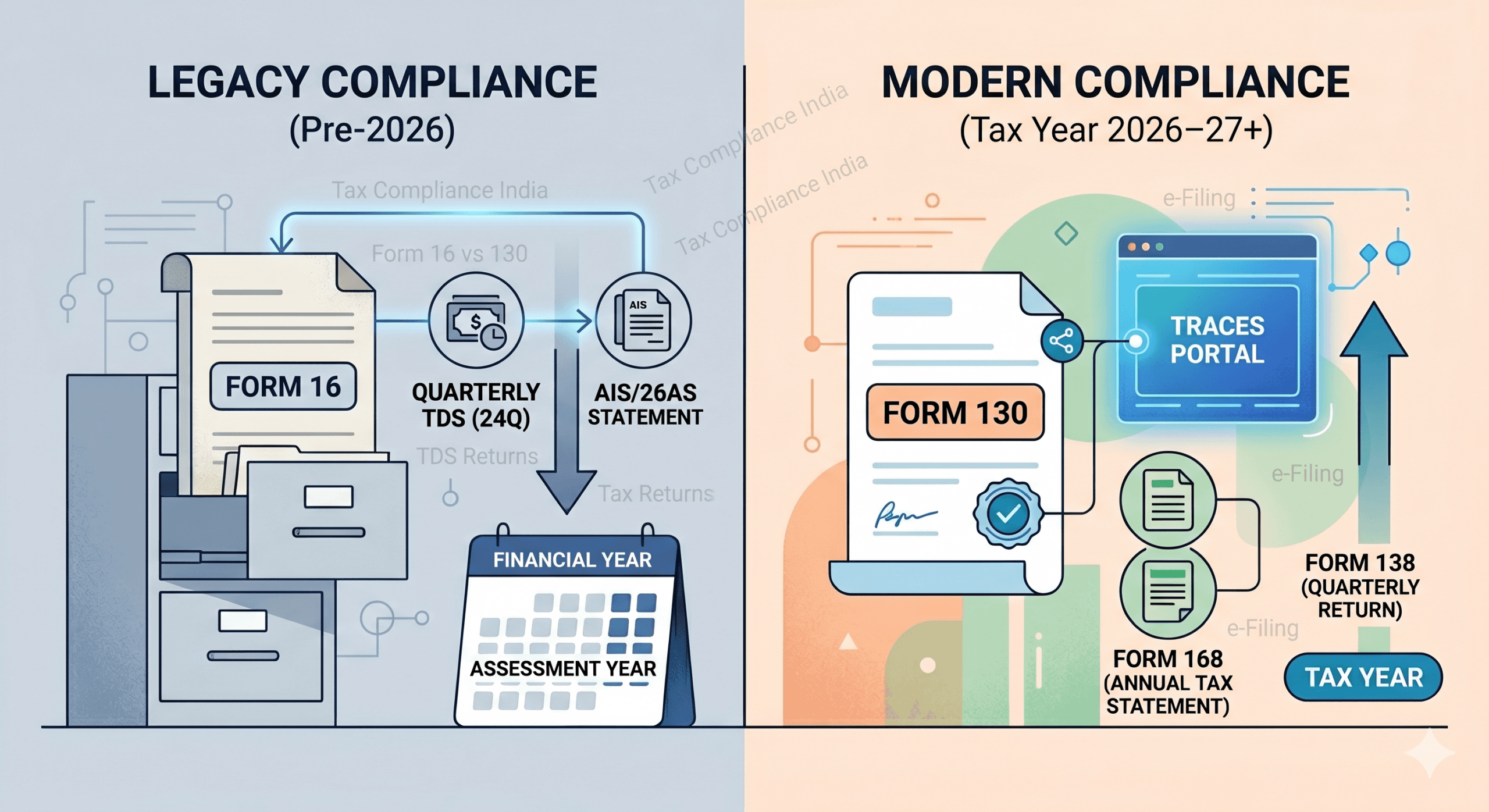

Decoding the Schema: The New Forms Translation Matrix

The central objective of the current Income Tax Rules is to eliminate administrative paperwork by standardizing tax filings. Out of roughly 399 legacy tax forms, the department has collapsed the system down to fewer than 190 digital formats.

To prevent internal filing errors, your HR operations and accounting desks must align on these updated statutory definitions:

| Legacy Form (Pre-2026) | New Form (Tax Year 2026–27) | Operational Purpose | Affected Corporate Desk |

| Form 16 | Form 130 | Annual Certificate of TDS on Salary | HR & Payroll |

| Form 24Q | Form 138 | Quarterly Salary TDS Returns | Finance & Payroll |

| Form 16A | Form 131 | TDS Certificate for Non-Salary Payments (Consultants/Vendors) | Accounts Payable |

| Form 26AS / AIS | Form 168 | Consolidated Annual Tax Statement (Employee View) | All Taxpayers / Workforce |

Critical Distinction for the 2026 Transition: During the current mid-2026 filing window, your team will still issue the legacy Form 16 to employees because it covers the historical financial year (FY 2025–26). However, for all salary paid and tax deducted from April 1, 2026 onward, the operational regime is strictly Tax Year 2026–27, and the mandatory compliance output will be Form 130.

Beyond the Label: What Makes Form 130 Structurally Different?

If your internal payroll software or manual Excel templates simply swap the title text from “Form 16” to “Form 130” without changing the data design underneath, your company risks issuing non-compliant certificates. Form 130 introduces an entirely new reporting framework:

1. The Shift to a Three-Part Architecture

While the traditional Form 16 relied on a twin-component structure (Part A for portal-derived tax deposits and Part B for internal salary computations), Form 130 introduces an explicit three-part format (Parts A, B, and C). This new annexure layout consolidates salary breakdowns, exemptions, deductions, and final liability directly within a system-verified interface, removing the need for manual calculations during tax season.

2. Mandatory Rate Disclosure and Real-Time TRACES Linking

Form 130 must be digitally processed and generated via the government’s TRACES portal. For the first time, it explicitly requires the disclosure of the exact tax deduction rate percentage. This allows employees to immediately see if their bonuses, special allowances, or monthly salaries were taxed at an incorrect slab rate, shifting the burden of absolute data accuracy upfront onto the employer.

3. The Eradication of “Assessment Year” Confusions

For decades, payroll teams had to manage the mental gymnastics of mapping a Financial Year (FY) to an Assessment Year (AY). The current framework completely eliminates this friction. Under the new rules, the period of income generation and reporting are unified under a single tag: Tax Year 2026–27.

[Old System]: Income Earned in FY 2024-25 ───> Reported in AY 2025-26 (High Friction)

[New System]: Income Earned in TY 2026-27 ───> Reported in TY 2026-27 (Unified Label)

The Operational Risk Matrix for Human Resources

When a regulatory change of this scale occurs, the primary point of failure is rarely intentional non-compliance—it is operational latency. CHROs must safeguard their business against three major internal risks:

- Software Misalignment: Legacy internal ERPs or outdated payroll setups that fail to map salary TDS to Section 392 of the new Act (which replaces the old Section 192) will generate broken, un-loadable quarterly files.

- The Employee Panic Loop: When employees review their updated tax statement online (Form 168), any lag or mismatched reporting in your quarterly Form 138 filings will trigger immediate internal inquiries, causing administrative gridlock for your HR support desk.

- The Compliance Lock-Out: Missing data points during quarterly submissions can stall the digital generation of Form 130 via TRACES, exposing the enterprise to structural late-issuance penalties.

The Executive Action Plan for HR Leadership

To ensure a seamless transition into the new tax compliance landscape, corporate leadership should implement a clear three-step operational roadmap:

1.Audit Internal Tech Stacks:Immediate Priority.

Review your internal payroll platform’s compliance specifications. Confirm that your vendor has fully updated their systems to output Form 130 structures and handle the revised data rules for Form 138 quarterly submissions.

2.Re-train Your Execution Desk:Next 15 Days.

Provide upskilling sessions for your compensation, benefits, and payroll personnel. Ensure they understand the transition to unified Tax Year labeling and the strict, system-driven fields required by the TRACES portal.

3.Deploy Proactive Internal FAQs:Pre-emptive Strategy.

Circulate internal corporate communications explaining the form changes to your employees. Informing your workforce ahead of time about the shift to Form 130 and Form 168 will prevent confusion during future tax filing seasons.

Turn Regulatory Friction into Operational Efficiency

Managing a scaling enterprise requires your HR leadership to focus entirely on talent acquisition, workplace productivity, and strategic growth—not navigating changing tax forms. Trying to re-engineer an internal payroll division to absorb complex structural tax updates often leads to unintended compliance issues.

This is where a dedicated compliance partner becomes a strategic asset.

At Payline, we act as an operational shield for corporate enterprises across India. Our comprehensive Payroll Outsourcing Services are designed to absorb every compliance update seamlessly. From building tax compliance rules directly into your monthly payroll cycles to generating perfectly reconciled Form 130 certificates and Form 138 returns, we handle the entire administrative burden.

Whether you are a scaling domestic business or setting up your very first entity via our India Entry and Business Registration division, Payline ensures your corporate operations remain unshakeable, compliant, and ahead of the curve.