After 64 years, the Income Tax Act, 1961 — with its 298 sections, 14 schedules, and thousands of judicial interpretations — is being replaced by the Income Tax Act, 2025. The new Act aims to simplify India's tax legislation by using plain language, removing redundant provisions, and restructuring the law for the modern economy. While the government has emphasised that the new Act is not intended to change tax rates or create new tax burdens, there are structural changes that every CFO of a company operating in India must understand.

1. The Language Is Simpler, But the Substance Remains

The most immediate change is the drafting style. Provisions that previously required cross-referencing multiple sections and sub-sections are now written in direct, functional language. For example, complex provisions around depreciation, deductions, and tax holiday calculations have been restructured into logical, self-contained units. For CFOs and finance teams, this means less time spent on interpretation and more time on application — in principle.

However, the simplification comes with a caveat: decades of judicial precedent were built on the specific wording of the 1961 Act. The new Act's altered language may trigger fresh rounds of litigation as taxpayers and the Revenue debate whether the intent of earlier judicial decisions survives the rewording. In the transition period, conservative interpretation is advisable.

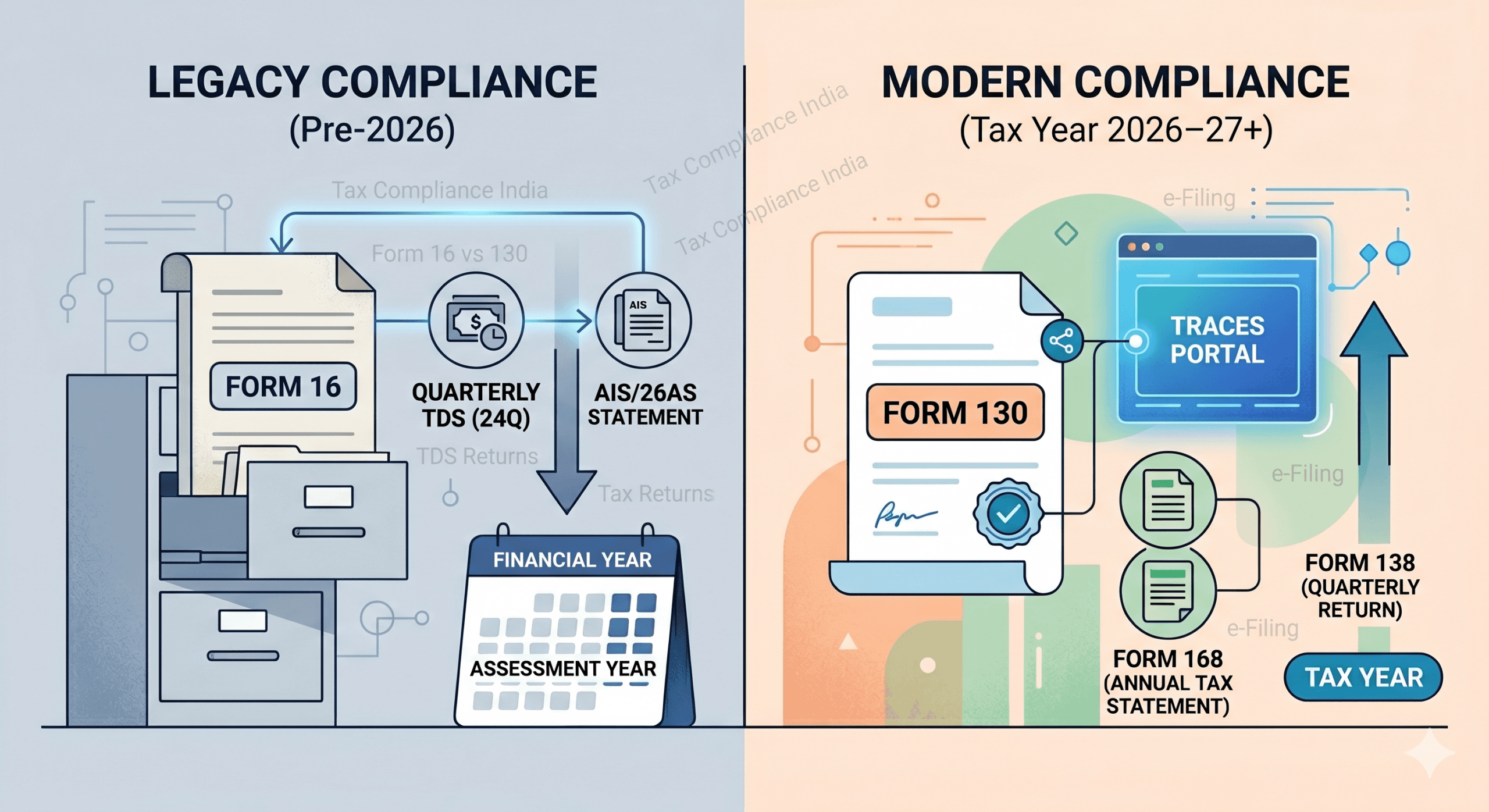

2. Tax Year Terminology Changes

The 2025 Act replaces the confusing "Previous Year" and "Assessment Year" terminology with a single concept: "Tax Year." Under the 1961 Act, income earned in the Previous Year (say, FY 2024–25) was assessed in the Assessment Year (2025–26). The new Act collapses this into a single Tax Year concept aligned with the financial year. This is a welcome simplification for multinational finance teams used to calendar-year reporting.

3. Transfer Pricing Provisions Are Substantially Unchanged

For UK companies with Indian subsidiaries, transfer pricing is always a key concern. The good news is that the core transfer pricing framework — arm's length pricing, documentation requirements, Advance Pricing Agreements (APAs) — is carried over substantially intact from the 1961 Act. The 2025 Act does not introduce new transfer pricing methods or change the primary adjustment and secondary adjustment rules.

However, the documentation threshold and related party definition provisions have been slightly restructured. Companies should review their existing transfer pricing documentation to ensure it maps correctly to the new Act's references rather than the old section numbers.

4. TDS Provisions Consolidated and Rationalised

One of the most operationally significant changes is the consolidation of TDS provisions. The 1961 Act had over 30 separate TDS sections (194, 194A, 194B, etc.), each with different rates, thresholds, and compliance requirements. The 2025 Act consolidates these into a more logical structure with a master table of TDS rates and thresholds, reducing the complexity of determining the applicable rate for a given payment.

For payroll specifically, TDS on salary (previously under Section 192) is now restructured under the new framework. Payroll systems must be updated to reference the new Act's provisions correctly — software vendors should release updates before the Act's effective date, but finance teams should verify compliance proactively.

5. The Transition Period Is a Compliance Risk Window

The transition from the 1961 Act to the 2025 Act creates a compliance risk window. Returns filed under the 1961 Act that are pending assessment will be processed under the old law. Disputes initiated under the old Act will continue under its provisions. New transactions from the effective date will fall under the 2025 Act. This dual-regime period demands that finance teams clearly document which legal framework applies to each transaction and assessment.

Payline Worldwide's India tax team provides expert guidance on navigating the transition to the Income Tax Act 2025. Our team helps UK-India businesses update their TDS processes, review transfer pricing documentation, and ensure compliance during the critical transition period. Contact us for a complimentary transition readiness assessment.